Just take my money, but please make it easy!

Paying for electric vehicle charging outside your usual spot can be a chore.

Don't always follow the example of the Nordic countries!

In Nordic countries, we have many electric vehicle apps for payment. In Norway, the number is close to 40 (being the most advanced electric vehicle market globally) and Sweden, Finland, Denmark and Iceland have their fair share as well and many with their own charger networks. The fair estimate is above 100!

Some charging providers offer roaming options to other networks, but usually at a significant cost. In practice drivers will install numerous apps, some of which charge an extra cost if no transactions are made in a given time.

Drivers don't like this. In our questionnaire of 413 Finnish electric vehicle drivers, 64% told us they'd rather use their existing multi-purpose payment apps (like Google Pay, Apple Pay, Vipps or MobilePay) for payment. 54% also preferred a credit card payment. Even early adopters of EVs regard multiple apps as bothersome.

The regulator has also taken note. The draft of the Alternative Fuels Infrastructure regulation explicitly requires an ad hoc payment option for all public electric vehicle charging stations and a credit card payment option at high-speed (DC) charging stations.

Credit cards seem the obvious choice for payment, but why are they not more common? One reason is that the charging networks want to create loyal users and become The Network in their area (the same reason roaming pricing is set so high).

Another and perhaps more important reason is the cost. Credit card terminals have an upfront cost of several hundred euros, their processing fees and transaction costs are significant and they need their network connections and device management solutions.

Most EVSEs are not even well suited to host credit card terminals; fitting them is mechanically laborious, chargers are not equipped to share their network connection and payment backends don't have existing integrations to charge point management systems.

Credit card payment is becoming more common, but for now, it's a quagmire of complexity and cost.

Still wouldn't it be nice if there was an easy way to pay for charging when outside your home network?

We have been thinking about this for a while, and here are the parameters to make end-users happy:

- Payment should be possible with existing payment methods

- No new app installations, no new tags

- No pre-registration and usable immediately

- No text/numeric input of any kind in a typical usage scenario

- The price and cost of the charging are visible to the user before and during the charging session

- Users can be sure that the charging is successful and they can follow it from the smartphone

- No manual selection or searching of charger

Also importantly, the charging network operator has a different set of needs:

- Installation of the new system at a charger should be doable in less than 5 minutes without more than 10 minutes of training

- For customers in our CPMS, the solution can be deployed in less than 1 week

- The solution is also available for networks that do not run on the eMabler Charge Point Management System

Anyone will agree this is a tall order.

Here's how we solved it.

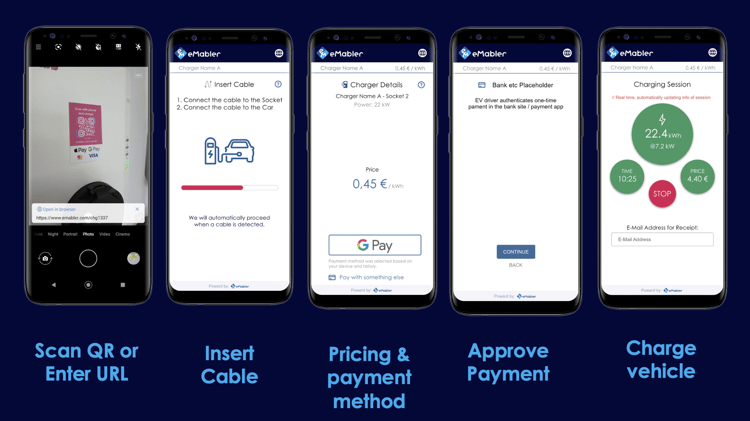

The above set of images shows the payment workflow, let's break it down:

- User scans a QR code or enters a short URL like emabler.com/chg1337 on their phone

- User is instructed to connect their car

We do this to ensure the right charger and show the right rates at multi-socket (AC/DC combo) chargers - User is shown pricing and offered to pay either with Google Pay or Apple Pay

We will support normal credit cards, but apps are superior to credit cards as they don't require separate authentication or input of details. - User accepts the payment

- User is shown a control view with an option to get a receipt to their email address.

In our tests, the flow takes about 7 seconds.

We still feel there are some improvements to be made.

We don't know what the transaction value will be at the start of the transaction, which means we may have to make a large reservation on the user's payment method at the start of the transaction, or risk running out of funds during it.

The obvious solution is familiar from the old school gas station terminal: We could add a screen to select the transaction amount, but that would mean adding an extra step in the transaction flow.

I refuse.

Instead, the solution is to adjust the payment pre-authorization amount based on the charger type (AC/DC) and usage pattern (90th percentile total transaction power), but this is still a bit crummy and issues too large reservations for most people. They get the money back of course, but it's still less than optimal.

That's why we work with the acquirer and payment processing partner and offer progressive preauthorization, which automatically creates multiple small preauthorizations on the user's payment method and adjusts the final one to match the transaction.

To further simplify the payment process we could include an NFC tag with the solution, which allows payment initiation by scanning the tag. The downside is that most iPhones still (in the year of our lord 2022) don't support scanning arbitrary tags. Still, Android phones account for about 70% of the market (in Europe and globally) and the hardware for NFC reading is present in approximately 59% of the global smartphone count, and much more prevalent in new phones.

In light of this, we work with a partner to offer combination tags that are low cost, easy to install and commission and mechanically suited for an outdoor environment.

All to shave off 2 seconds from the payment flow.

We have a few other ideas too, but the law of diminishing returns applies here.

Would you take this into use in your charging network? Book a meeting with me, and let's get started!

Frequently Expected Questions (or... FEQ?)

Good job. I still want to use a credit card terminal instead.

We don't blame you and we also support credit card payments. Have you followed the development in payments in general? Credits cards will be a history and people pay with their smartphones.

You are fools. EMP apps and NFC tags are king.

We agree that EV drivers will likely have a home network which has an app and a tag (or plug & charge certificate). Paying outside your normal network is still relatively common especially in central Europe where people drive regularly their cars to other countries.

You are fools. ISO15118's Plug & Charge will kill ad hoc payment.

Plug & Charge does not mitigate the need for having a contract with the EMPs present at the charger. But it will provide some other nice use case. More about those later.

You are fools, roaming will solve all.

We yearn for a time when all that is in place and we can sunset this concept. In fact we work to make it so with various roaming hubs and direct roaming contracts.

Could this be used in apartment or office charging?

We imagine that convenience is king in the daily scenario.

About the author:

Visa Parviainen - Chief Product Officer

Visa is a business technologist with a diverse background in software and hardware, including IoT, electromobility and business development.

eMabler

Based in Helsinki, Finland. We believe that eMobility is the way forward, having worked in the industry for over a decade and we see a great boom in eMobility. We’ve also seen many platform providers develop closed ecosystems and realized that there’s a need for a more flexible solution that focuses on end-user experience.

That’s why we decided to build an open platform that lets you integrate your EV charging data into any existing systems, please contact us.

COMMENTS